EPC, OC, HoldCo, and PropCo: Know the Difference

Business buyers and real estate investors often use entity labels as though they are interchangeable.

They are not.

An SBA Eligible Passive Company is not automatically a conventional holding company. An Operating Company under SBA rules may also be an OpCo for legal and accounting purposes, but the terms arise from different questions. A real estate entity may be called a PropCo, property LLC, holding company, or EPC depending on the context.

This creates room for expensive misunderstandings.

Your lender may use one term to describe loan eligibility. Your attorney may use another to explain liability separation. Your accountant may focus on the entity’s tax classification. Your internal acquisition model may use HoldCo and OpCo only to show ownership.

All four perspectives can be valid while describing different features of the same structure.

Learn How Better Landlords Manage Better Rentals

Join our 2X weekly newsletter for clear, actionable guidance on property management, leasing, tenant issues, rental property operations, and real estate investing strategies you can actually use.

Begin With the SBA Terms

SBA financing is intended for eligible operating small businesses. Passive businesses are generally ineligible, but SBA rules permit a qualifying Eligible Passive Company to own property and lease it to an eligible Operating Company under prescribed conditions.

SBA Form 1919 describes an EPC as a qualifying entity or trust that does not conduct regular and continuous business activity and leases real or personal property to an Operating Company for use in the OC’s business.

A simplified structure may look like this:

- EPC: Owns the commercial real estate.

- OC: Operates the service business from the property.

- Lease: Governs the OC’s use of the EPC-owned property.

- Owners: Hold interests in the entities as permitted by SBA requirements.

- Lender: Takes the required guarantees, liens, and assignments.

The EPC exception allows the transaction to separate property ownership from operations without turning the real estate owner into an ineligible passive investment borrower.

But the arrangement must comply with current SBA rules.

The current SBA lending SOP contains the controlling loan-origination policies for 7(a) and 504 lenders.

What the EPC Is Not

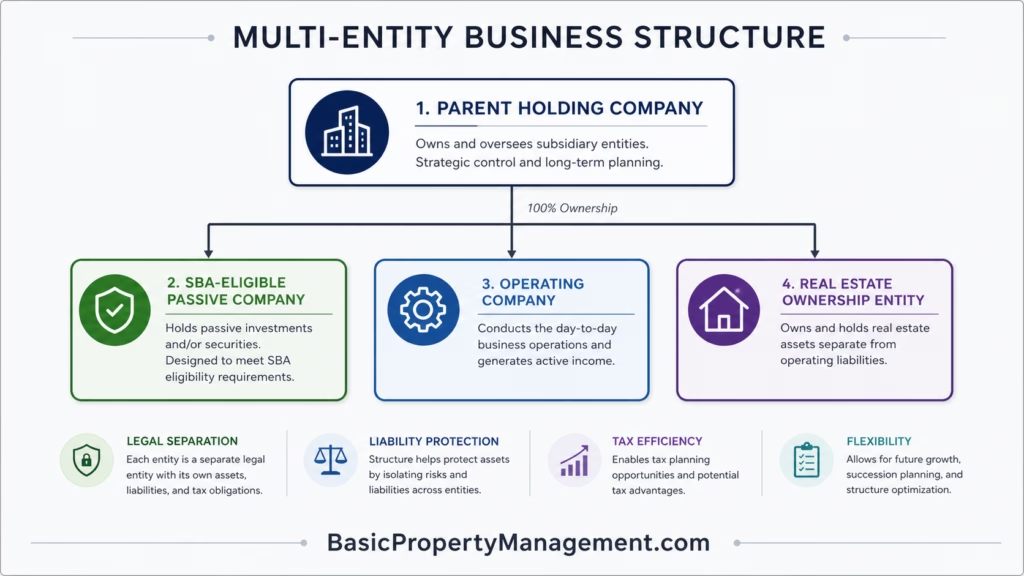

An EPC is not automatically a parent company.

A parent holding company generally owns equity interests in one or more subsidiaries. An EPC generally owns eligible property that it leases to an Operating Company.

Those roles can overlap only if the resulting ownership and financing arrangement satisfies the applicable legal, tax, and SBA requirements. You should not create a parent entity, call it the EPC, and assume the structure qualifies.

An EPC is also not a general real estate investment company.

Its purpose in an SBA transaction is tied to property used by the eligible Operating Company. SBA financing cannot be used to create a conventional passive rental investment merely because the tenant and landlord have common ownership.

The EPC does not automatically protect the property from operating-company creditors either. Entity separation may help, but guarantees, mortgages, assignments of rent, cross-defaults, and lender liens can connect the entities economically.

HoldCo Describes Ownership

A holding company generally owns interests in other entities rather than conducting the main day-to-day operations itself.

For a multi-acquisition strategy, a HoldCo may own:

- Operating Company A

- Operating Company B

- A shared-services company

- Intellectual property

- One or more real estate entities

- Other investment subsidiaries

The HoldCo can provide centralized ownership, governance, and capital allocation.

But adding a holding company creates additional questions:

- Will the SBA lender permit the proposed ownership chain?

- Which entity will guarantee the loan?

- Will affiliation rules affect SBA eligibility?

- Can distributions move from the operating entity to HoldCo?

- Does the loan agreement restrict dividends or management fees?

- Will future investors enter at the parent or subsidiary level?

- Can one acquisition be sold without disturbing the others?

A HoldCo may simplify ownership on a chart while adding tax returns, state filings, bank accounts, intercompany agreements, and reporting responsibilities.

The structure should solve a defined problem.

OpCo Describes Operations

An OpCo performs the business activity.

It may:

- Employ workers

- Sign customer contracts

- Bill clients

- Maintain operating licenses

- Buy inventory

- Lease vehicles

- Hold vendor relationships

- Manage the business name

- Earn operating revenue

In an SBA-financed transaction, the OpCo may also be the SBA Operating Company.

However, the legal abbreviation “OpCo” does not itself establish SBA eligibility. The lender must evaluate the actual business, ownership, loan use, affiliation, occupancy, and other requirements.

The Operating Company may also guarantee or become a co-borrower on an EPC loan, depending on the transaction and use of proceeds. SBA loan documents specifically account for EPC/OC structures and require the lender to address both entities.

PropCo Describes Property Ownership

A PropCo owns real estate.

It may receive rent from the operating company and pay:

- Mortgage debt

- Property taxes

- Building insurance

- Structural repairs

- Capital improvements

- Property-level professional fees

A separate PropCo can make it easier to understand the performance of the real estate independently from the operating business.

It may also create flexibility later. You could sell the operating company and retain the property as a landlord, sell the property and relocate the business, or refinance the real estate separately.

Those outcomes depend on the loan documents and transaction structure. A separate entity does not guarantee the freedom to transfer or refinance the property.

When SBA financing is involved, the PropCo may need to function as the EPC and comply with the related lease, guarantee, occupancy, and ownership requirements.

The Lease Must Be Real

An intercompany lease should not exist only because the closing checklist requires one.

It should address:

- Premises

- Lease term

- Renewal options

- Rent

- Additional rent

- Utilities

- Property taxes

- Insurance

- Maintenance

- Structural repairs

- Capital improvements

- Alterations

- Assignment

- Subordination

- Default

- Damage and condemnation

- Lender-required provisions

SBA documentation requires a written EPC-to-OC lease with terms that align with the loan requirements. For example, SBA eligibility materials contemplate a remaining lease term at least equal to the loan term, including qualifying renewal options, and subordination to the SBA lien.

The rent also matters for tax and operating analysis.

Rent that is too high may weaken the operating company and artificially shift income to the real estate entity. Rent that is too low may understate property performance and create questions about arm’s-length treatment.

Your attorney, lender, appraiser, and tax adviser should review the lease from their respective perspectives.

SBA Structure Does Not Decide Tax Classification

This is the distinction buyers most often miss.

An SBA-compliant EPC/OC arrangement does not determine whether the real estate rental activity is passive, nonpassive, or grouped with the operating business for federal income-tax purposes.

Those questions arise under Section 469 and its regulations.

A landlord may rent property to an operating business in which the same taxpayer materially participates. The self-rental rules can recharacterize certain net rental income as nonpassive. A rental loss may remain passive unless the activities are validly grouped or another rule applies.

Under the federal activity-grouping regulations, taxpayers may group activities that form an appropriate economic unit, but special restrictions apply when combining rental and operating activities.

You therefore need to answer two separate questions:

- Does the entity and lease structure comply with SBA requirements?

- How should the activities be treated for federal tax purposes?

Our article Self-Rental Rules Can Trap Your Depreciation addresses the second question.

A Structure Can Be Legally Separate but Economically Connected

Suppose the real estate sits in Property LLC and the operating business sits in Service Company LLC.

The entities may have:

- Separate formation documents

- Separate tax identification numbers

- Separate bank accounts

- Separate financial statements

- A written lease

But they may also share:

- The same owners

- Personal guarantees

- Cross-default provisions

- Cash-flow dependence

- Lender collateral

- Insurance programs

- Management personnel

- Tax groupings

The separation remains useful, but you should understand its limits.

The property is valuable because the operating company can pay rent. The operating company is valuable partly because it controls its location. A failure in either entity may affect the other.

This is why your acquisition model should include separate and combined financial statements.

Keep the Structure as Simple as the Strategy Allows

Before adding an entity, identify its specific job.

A practical first acquisition might require:

- One real estate entity

- One operating company

- A written lease

- A parent holding company only when it solves a real ownership or acquisition problem

More entities may be appropriate when you have multiple owners, different asset groups, regulated licenses, shared services, or a defined acquisition pipeline.

But complexity carries a cost.

Every entity may require:

- Formation and annual fees

- Accounting

- Tax filings

- Bank accounts

- Insurance

- Contracts

- Governance records

- State registrations

- Lender approval

- Intercompany reconciliations

A structure that saves a theoretical amount of liability or tax can lose money through poor administration.

Design Around the Exit as Well as the Closing

Ask what you expect to happen in five or ten years.

You may want to:

- Sell the operating business but retain the real estate.

- Sell the property to the operating-business buyer.

- Add another operating company.

- Bring in a minority investor.

- Transfer ownership to family members.

- Refinance the property.

- Centralize management.

- Acquire a competitor.

- Sell the entire group.

The entity structure should not block the most likely outcomes.

It should also acknowledge that SBA and other acquisition loans may restrict ownership transfers, additional debt, distributions, management fees, guarantees, and changes in control.

The article Build the First Deal for a Future Acquisition discusses how to plan for later transactions.

Use the Correct Term for the Correct Question

Use EPC and OC when addressing SBA eligibility and loan structure.

Use PropCo and OpCo when describing ownership of real estate and business operations.

Use HoldCo when describing a parent that owns subsidiary interests.

Then separately determine each entity’s tax classification, legal role, liability exposure, and reporting responsibilities.

The labels are useful. They are not the structure itself.

A sound structure should satisfy the lender, support the operating business, preserve appropriate separation, produce workable tax reporting, and remain understandable to the people who must manage it after closing.