Rental Property Owner Statements Explained

Rental property owner statements are one of the most important financial reports a landlord receives from a property manager. They show what happened financially during the reporting period: rent collected, expenses paid, management fees deducted, reserves held, and money distributed to the owner.

For landlords who use professional property management, the owner statement is the monthly checkpoint for the investment. It is not enough to glance at the deposit amount and move on. The real value of the statement is in understanding how the property performed, whether the numbers make sense, and whether any issues need attention.

A well-prepared owner statement should answer several practical questions. Was rent collected in full? Were any late fees, pet fees, or reimbursements received? What repairs were completed? Were the expenses reasonable? Did the manager hold back a reserve? How much cash was distributed to the owner? Is the property producing stable income or quietly drifting into negative cash flow?

This in-depth guide explains what rental property owner statements usually include, how landlords should read them, and the red flags that may signal accounting problems, weak property management, or declining rental performance.

Get Practical Property Management Tips Twice a Week

Want smarter systems for managing rentals, screening tenants, handling maintenance, and improving property performance? Sign up for our 2X weekly newsletter and get practical property management and real estate investing insights delivered straight to your inbox.

What Are Rental Property Owner Statements?

A rental property owner statement is a financial report prepared by a property manager for the rental owner. It summarizes income, expenses, fees, reserves, owner contributions, owner distributions, and account balances for a specific period.

Most owner statements are issued monthly. Some property managers also provide quarterly summaries, year-end statements, rent rolls, income statements, maintenance reports, and tax documents through an owner portal.

At a basic level, the owner statement should show money in and money out. That sounds simple, but the details matter. A statement that only shows a deposit amount does not give the owner enough information to evaluate the property.

A strong owner statement should help the landlord understand both cash movement and operating performance.

Owner Statement vs. Profit and Loss Statement

An owner statement and a profit and loss statement are related, but they are not always the same report.

A profit and loss statement focuses on income and expenses over a period. It helps show whether the property operated profitably before considering certain balance sheet items, reserves, or owner distributions.

An owner statement often includes more cash-flow detail. It may show rent collected, expenses paid, management fees, repair charges, reserve balances, owner contributions, and the final owner distribution.

That distinction matters. A property may show positive income for the month but still produce a smaller owner distribution because the manager held back funds for reserves, paid a large vendor invoice, deducted a leasing fee, or carried forward a prior negative balance.

Owner Statement vs. Rent Roll

A rent roll is different from an owner statement.

The rent roll shows lease-level and tenant-level information. It usually includes tenant names, unit numbers, rent amounts, lease dates, security deposits, balances, and occupancy status.

The owner statement shows the owner’s financial activity. It may show rent collected, but it usually does not replace the rent roll. For multi-unit properties, landlords should review both reports. The rent roll tells the owner what should have been collected. The owner statement shows what was actually collected and paid out.

Why Owner Statements Matter

Rental property owner statements matter because they help landlords monitor financial performance without managing every day-to-day task themselves.

A rental can look stable from the outside while the numbers tell a different story. A tenant may be paying late every month. Repairs may be increasing. The manager may be charging fees the owner did not expect. A reserve may be growing without explanation. A property may be producing less cash flow than projected.

The owner statement is where many of these issues first appear.

Owner Statements Help Verify Cash Flow

The owner statement should help the landlord see whether the property produced positive or negative cash flow during the reporting period.

This is especially important when the owner pays some expenses outside the property manager’s system. For example, the manager may collect rent and pay repairs, but the owner may personally pay the mortgage, property taxes, insurance, or HOA dues.

In that case, the owner statement may show a positive distribution even though the property’s true cash flow is lower after the owner’s direct expenses are considered.

Owner Statements Support Tax Preparation

Rental property owner statements also help with tax preparation. The IRS explains that rental income generally must be reported and that many rental-related expenses may be deductible, depending on the circumstances. Clear records make it easier to separate rent, repairs, management fees, utilities, insurance, taxes, and other expenses when preparing a return. Landlords can review the IRS overview on rental real estate income, deductions, and recordkeeping for general federal guidance.

Monthly owner statements should not replace tax advice. They should, however, make tax preparation easier by keeping income and expense records organized throughout the year.

Owner Statements Help Evaluate the Property Manager

A property manager’s owner statement also tells the landlord something about the manager’s operating discipline.

Clear statements, timely reporting, accurate categories, invoice support, and prompt answers to questions suggest a manager with organized accounting controls. Confusing statements, delayed reporting, unexplained charges, and inconsistent classifications may indicate deeper management problems.

Landlords should not assume every unclear item is improper. But they should expect the manager to explain the numbers clearly.

What Rental Property Owner Statements Usually Include

Owner statement formats vary by company and software platform, but most include the same core categories.

Statement Period and Property Information

The statement should clearly identify the reporting period. For example, it may cover April 1 through April 30 or May 1 through May 31.

It should also identify the owner, property address, unit number if applicable, and sometimes the management company or account name.

This matters because landlords with multiple rentals need to know which income and expenses belong to which property. If the owner statement combines multiple units or properties, the report should still allow the landlord to see activity by property or unit.

A statement covering an unusual period should be reviewed carefully. A partial month, move-in month, move-out month, or correction period may not compare cleanly to prior statements.

Beginning Balance

The beginning balance shows the cash balance carried into the statement period. This may include funds held for reserves, prior unpaid bills, undistributed owner funds, or a previous negative balance.

The beginning balance should generally match the ending balance from the prior statement. If it does not, there may be a timing adjustment, voided transaction, corrected entry, bank reconciliation adjustment, or prior-period correction.

That is not automatically a problem. But the manager should be able to explain the difference.

Rental Income Collected

Rental income is usually the largest income item on the owner statement. It should show rent collected during the reporting period.

Depending on the format, rental income may appear as a single total or may be broken down by tenant, unit, payment date, or lease charge.

Landlords should compare collected rent against expected rent. If the lease says the tenant owes $1,800 per month, the statement should make it clear whether the full $1,800 was collected.

If collected rent is lower than expected, the reason should be identifiable. Common explanations include vacancy, prorated rent, partial payment, late payment, move-in adjustment, tenant credit, concession, or delinquency.

Other Income

Other income may include late fees, pet rent, utility reimbursements, parking charges, laundry income, storage fees, tenant repair reimbursements, lease violation fees, or other charges.

This section deserves attention because not all extra income is handled the same way. Some management agreements allow the property manager to keep certain fees. Others pass those fees to the owner.

For example, late fees may belong to the owner, the manager, or be split between the two depending on the management agreement. Application fees are often retained by the manager or used to cover screening costs. Lease renewal fees may be charged to the owner rather than the tenant.

The statement should be consistent with the lease and the management agreement.

Management Fees

Management fees are the charges paid to the property manager for ongoing management. They may be calculated as a percentage of rent collected, a flat monthly fee, or another agreed structure.

Landlords should verify that the management fee matches the contract.

If the management fee is 8% of collected rent and the tenant paid $2,000, the fee would usually be $160. If the tenant paid only $1,000, the fee may be $80 if the agreement is based on collected rent. Some contracts, however, use rent due or another calculation method.

The owner should know the difference. A management fee based on rent collected is not the same as a fee based on rent scheduled.

Leasing Fees and Renewal Fees

Leasing fees are usually charged when a manager places a new tenant. Renewal fees may apply when an existing tenant signs a lease extension.

These charges can materially reduce the owner distribution in the month they occur. They are not necessarily red flags, but they should be expected.

The owner statement should make it clear when the fee was charged and why. The amount should match the management agreement, and the landlord should be able to connect the charge to a signed lease, renewal, or tenant placement event.

Maintenance and Repair Expenses

Maintenance and repair expenses are often the most scrutinized part of the owner statement. They may include plumbing, HVAC, electrical work, appliance repair, landscaping, pest control, cleaning, locksmith services, painting, turnover work, or general handyman charges.

A good owner statement should describe repairs clearly enough for the owner to understand what happened. “Maintenance – $725” is not very useful. “Replace leaking toilet supply line and reset toilet, Unit 2B – Invoice 1194” is much better.

Large repairs should have invoice support. Many property management systems allow managers to share reports, work orders, inspection documents, and owner records through online portals. For example, Buildium describes property management reporting as a way to track rental income, expenses, and other key metrics through accounting and management tools. Landlords can use that kind of reporting framework as a benchmark for what organized property reporting should provide. Buildium’s property management reporting overview is a useful example of the reports owners may expect from a manager using modern software.

The larger the repair, the more documentation the owner should expect.

Utilities, HOA Fees, Taxes, and Insurance

Some property managers pay property-related bills on behalf of the owner. These may include utilities, HOA dues, insurance, city rental registration fees, trash service, lawn care, pest control, or property taxes.

Other expenses may be paid directly by the owner and never appear on the statement.

This distinction is important. A property may look profitable on the owner statement because the manager’s report does not include the mortgage, insurance, property taxes, or HOA dues paid outside the management account.

For a complete view of performance, the landlord should combine the owner statement with any owner-paid expenses.

Owner Contributions

An owner contribution is money sent by the landlord to the property manager. This usually happens when the property account does not have enough cash to cover expenses, required reserves, or repairs.

One owner contribution may be normal after a major repair or during a turnover month. Repeated owner contributions are different. They may indicate a property that is not generating enough operating cash to support itself.

Possible causes include high vacancy, below-market rent, recurring repairs, weak tenant screening, excessive fees, or a property that was undercapitalized from the beginning.

Reserves

Many property managers require an owner reserve. This is money held in the property account to cover repairs, bills, or emergency expenses.

For example, a manager might require a $500 reserve for a single-family rental. A larger or older property may require more.

Reserves reduce owner distributions because the money is held rather than paid out. That is not inherently bad. A reasonable reserve helps the manager handle routine expenses without requesting owner approval for every small item.

The reserve should match the management agreement. If the reserve increases, the owner should understand why.

Owner Distributions

The owner distribution is the amount sent to the landlord after income, expenses, fees, reserve requirements, and adjustments are accounted for.

This is the number many owners check first, but it should not be read alone. A lower-than-expected distribution may be caused by unpaid rent, repairs, leasing fees, reserve holdbacks, prior negative balances, vacancy, or timing differences.

Before assuming there is a problem, compare the distribution to the income, expense, and reserve sections.

Ending Balance

The ending balance shows the remaining cash balance at the end of the reporting period. It may include reserves, unpaid owner funds, held funds for bills, or a negative balance owed by the owner.

The ending balance should become the beginning balance on the next statement. If it does not, the landlord should ask for clarification.

How Landlords Should Read Rental Property Owner Statements

Reading owner statements should be a monthly habit. The review does not need to be complicated, but it should be consistent.

Step 1: Confirm the Reporting Period

Start with the dates. Make sure the statement covers the month or period expected.

A partial month can distort income and expenses. This commonly happens during tenant move-in, tenant move-out, new management onboarding, or accounting corrections.

What to ask

Does this statement cover the full period I expected?

If not, what dates are included and why?

Step 2: Compare Scheduled Rent to Collected Rent

Next, review rental income. Compare the rent collected to the rent that should have been collected under the lease.

For multi-unit properties, review this by unit. A total rent number may hide one delinquent tenant if other tenants paid on time.

What to ask

Was all rent collected in full?

If not, which tenant is short, how much is owed, and what is the collection plan?

Step 3: Review Non-Rent Income

Check late fees, pet rent, utility reimbursements, parking charges, and tenant reimbursements.

These amounts may seem small, but they can affect annual returns. They also reveal whether the manager is enforcing lease terms consistently.

What to ask

Are all recurring tenant charges being billed correctly?

Are tenant reimbursements collected when tenants are responsible for damage or utilities?

Step 4: Read Every Expense Line

Every expense line should be understandable. The landlord should know what was paid, who was paid, and why.

That does not mean the owner should challenge every $75 charge. It means the statement should contain enough information to make the charge understandable.

What to ask

Do I understand what this expense was for?

Is there an invoice or work order for larger charges?

Was owner approval required under the management agreement?

Step 5: Separate Routine Expenses From One-Time Expenses

A normal month may include management fees, small repairs, landscaping, pest control, or utility charges.

A non-routine month may include a leasing fee, turnover work, roof repair, appliance replacement, insurance payment, property tax payment, or reserve increase.

This distinction helps owners interpret the statement correctly. One high-expense month may not mean the property is underperforming. Repeated high-expense months may indicate a larger issue.

What to ask

Is this a recurring expense, seasonal expense, turnover expense, or one-time repair?

Step 6: Compare Distribution to True Cash Flow

The owner distribution is not always the same as the property’s true cash flow.

To understand actual cash flow, landlords should subtract owner-paid expenses that do not appear on the statement. These may include mortgage payments, property taxes, insurance, HOA dues, asset management fees, bookkeeping costs, or major capital expenditures paid directly by the owner.

Mortgage lenders often analyze rental income by subtracting regular and ongoing expenses such as maintenance, advertising, management fees, utilities, HOA dues, and supplies from rental cash flow. Fannie Mae’s guidance on income or loss reported on Schedule E illustrates how important full expense visibility can be when evaluating rental performance.

What to ask

After all owner-paid expenses, did the property actually produce cash flow this month?

Step 7: Track Trends Over Time

One statement is a snapshot. Several statements show a pattern.

Owners should compare statements across multiple months. The most useful trends include rent collection, maintenance costs, vacancy, management fees, owner distributions, reserve balances, and owner contributions.

A single $900 repair may not be alarming. A $900 repair every month deserves closer review.

Red Flags in Rental Property Owner Statements

Not every unusual number is a problem. Rental properties are operational assets, and expenses fluctuate. But certain patterns deserve attention.

Vague Expense Descriptions

Expense descriptions such as “maintenance,” “repairs,” “supplies,” or “vendor charge” are too vague when the amount is meaningful.

For small charges, a general label may be tolerable. For larger charges, the statement should describe the work performed, the property or unit affected, and the vendor involved.

Why it matters

Vague expenses make it difficult to verify whether the charge is legitimate, reasonable, and allocated to the correct property.

What to do

Ask for the invoice, work order, vendor name, completion date, and repair description.

Missing Invoices for Larger Repairs

A property manager should be able to provide invoices for repair charges, especially when the amount exceeds the owner approval threshold.

Why it matters

Invoices help verify what work was completed, when it was completed, who performed it, and whether the amount matches the statement.

What to do

Ask whether invoices are uploaded to the owner portal and whether all charges over a certain amount require documentation.

Management Fees That Do Not Match the Agreement

Management fees should follow the signed management agreement.

A mismatch may be an innocent accounting error. Repeated mismatches are more concerning.

Why it matters

Incorrect fee calculations can reduce owner returns over time. They may also indicate weak internal controls.

What to do

Ask the manager to show the calculation and point to the applicable section of the management agreement.

Rent Collected Is Lower Than Expected Without Explanation

Lower rent collection can be legitimate. It may reflect a vacancy, move-in proration, tenant delinquency, concession, or partial payment.

The issue is not simply that rent is lower. The issue is when the statement does not explain why.

Why it matters

Unexplained rent shortfalls can hide collection problems, tenant issues, accounting errors, or unreported vacancy.

What to do

Ask for the tenant ledger and a written status update on any unpaid balance.

Repeated Owner Contributions

One owner contribution may be normal after a large repair or during a tenant turnover. Repeated contributions are a stronger warning sign.

Why it matters

Frequent contributions may mean the rental is not financially self-sustaining.

What to do

Ask for a trailing 12-month income and expense report. Review rent, vacancy, maintenance, fees, utilities, and recurring expenses.

Negative Ending Balances

A negative ending balance means the property account is short.

This may happen after a major repair, delayed rent payment, vacancy, or reserve adjustment. It should not be ignored.

Why it matters

A negative balance may prevent bills from being paid and may require an owner contribution.

What to do

Ask what caused the negative balance and what amount is needed to bring the property account current.

Frequent Corrections, Reversals, or Reclassifications

Occasional accounting corrections happen. Frequent reversals, deleted charges, reclassified expenses, or unexplained adjustments are different.

Why it matters

Repeated corrections may indicate weak bookkeeping, poor reconciliation, software misuse, or lack of review before statements are issued.

What to do

Ask whether statements are finalized after bank reconciliation and who reviews owner statements before distribution.

Expenses Allocated to the Wrong Property

Owners with multiple properties should watch for misallocated expenses.

A plumbing repair at one address should not appear on another property’s statement. Shared expenses should be clearly labeled and allocated consistently.

Why it matters

Misallocated expenses distort performance and may cause one property to subsidize another.

What to do

Ask for property-level detail and vendor invoices.

Unexplained Reserve Increases

Reserves are normal, but they should not change without a clear reason.

Why it matters

An unexplained reserve increase reduces owner distributions and may signal upcoming expenses the owner has not been told about.

What to do

Ask why the reserve changed and whether the change is temporary or permanent.

Late or Inconsistent Statements

Owner statements should arrive on a predictable schedule.

A one-time delay may not matter. Repeated delays can interfere with cash-flow planning, tax preparation, and owner oversight.

Why it matters

Late statements may indicate slow accounting close, unreconciled accounts, staffing problems, or disorganized back-office processes.

What to do

Ask when statements are finalized each month and when owner distributions are processed.

Learn How Better Landlords Manage Better Rentals

Join our 2X weekly newsletter for clear, actionable guidance on property management, leasing, tenant issues, rental property operations, and real estate investing strategies you can actually use.

Questions Landlords Should Ask Their Property Manager

A landlord does not need to interrogate every line item. But a good property manager should be able to answer reasonable financial questions clearly.

Before signing a management agreement, or when reviewing reporting quality, ask:

- When are owner statements issued each month?

- Are statements prepared on a cash basis or accrual basis?

- What reports are included with the monthly owner packet?

- Are invoices uploaded for maintenance charges?

- What repair amount requires owner approval?

- How is the owner reserve calculated?

- How are management fees calculated?

- Are late fees retained by the manager, paid to the owner, or split?

- How are tenant balances reported?

- Can I receive a rent roll with the owner statement?

- Can I export income and expense reports for tax preparation?

- Who should I contact if a statement has an error?

These questions help set expectations before frustration develops.

Reports That Should Support the Owner Statement

A monthly owner statement is important, but it should not be the only financial report a landlord receives. The right supporting reports make the statement easier to verify.

The rent roll shows scheduled rent, lease dates, tenant balances, deposits, occupancy, and unit-level information.

This helps landlords compare what should have been collected against what was collected.

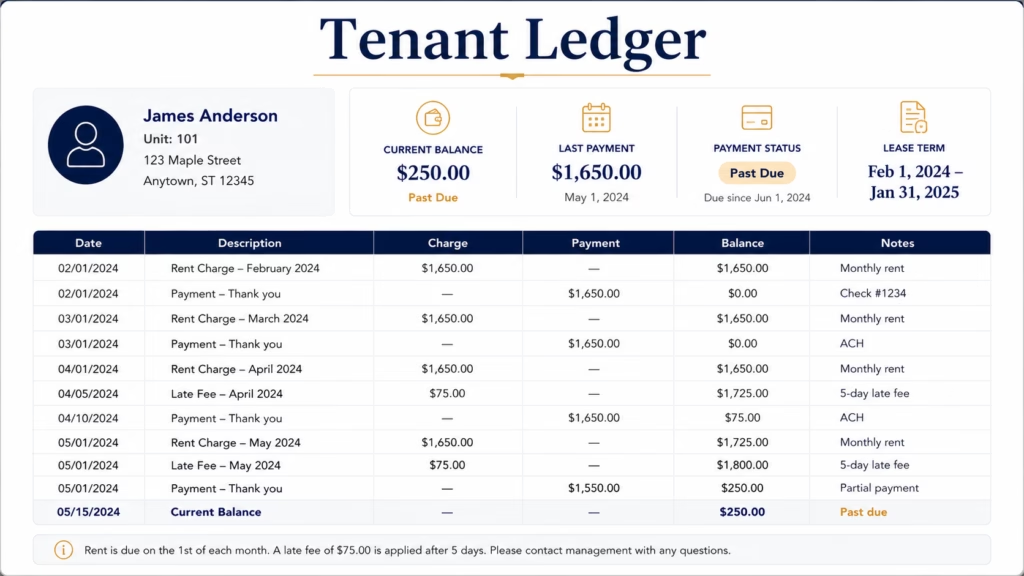

A tenant ledger shows charges, payments, credits, and balances for a specific tenant.

This is useful when rent is short, late fees are disputed, or a tenant has a running balance.

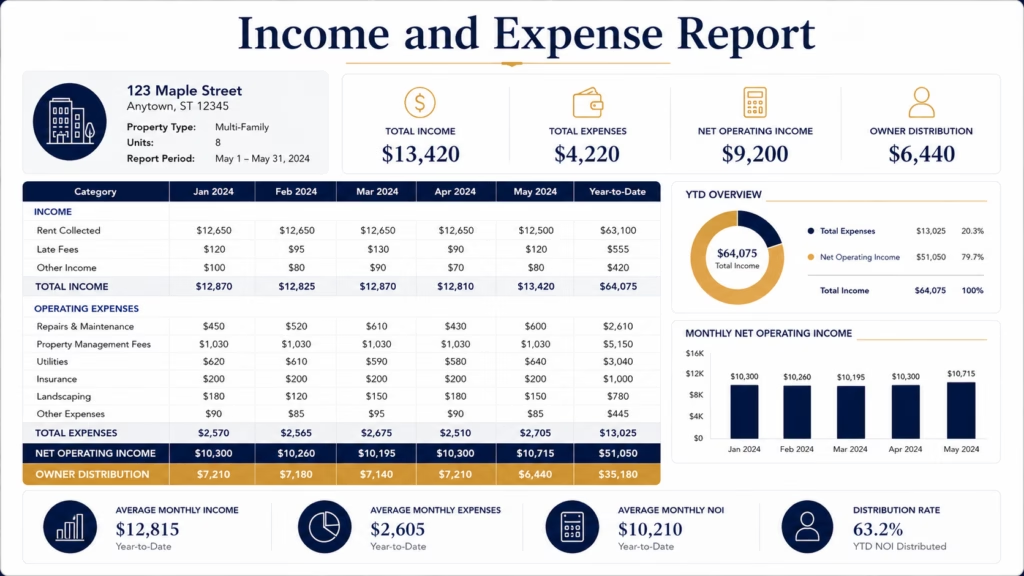

An income and expense report helps owners review operating performance over a period, such as month-to-date, quarter-to-date, or year-to-date.

This report is especially useful for identifying trends.

A maintenance report shows open work orders, completed repairs, vendor activity, recurring issues, and sometimes photos or inspection notes.

This helps owners understand whether repair costs are isolated or part of a broader pattern.

The owner ledger shows owner contributions, distributions, reserve changes, and balances.

This is useful when the owner wants to understand why the distribution does not match net income.

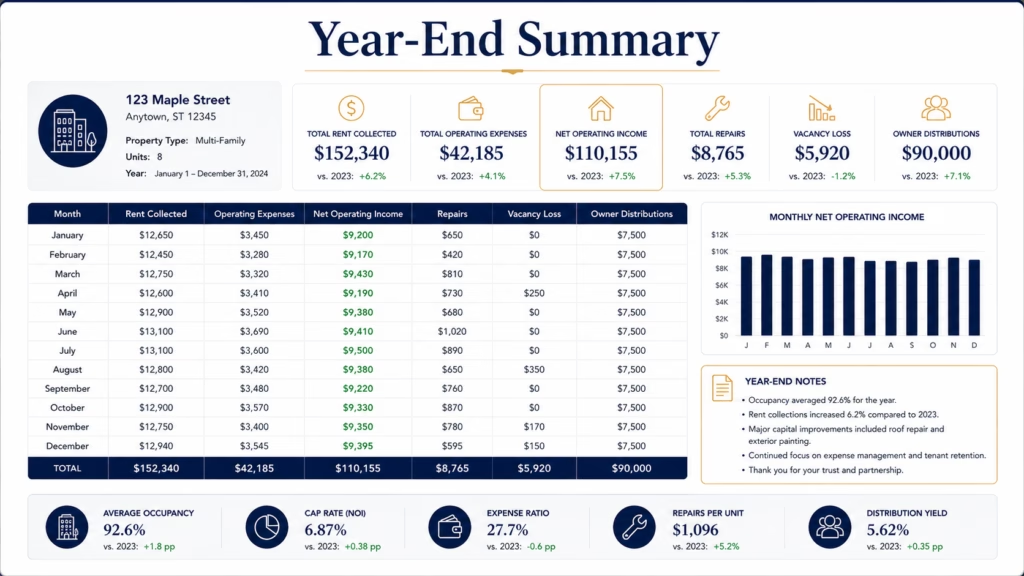

A year-end summary helps organize income and expense records for tax preparation. It should be consistent with the monthly statements issued throughout the year.

How Owner Statements Help Landlords Make Better Decisions

Owner statements are more than accounting records. Used properly, they help landlords make operational and investment decisions.

Rent Pricing

If income is consistently below expectations, the owner may need to review rent pricing, renewal strategy, concessions, vacancy loss, or local market conditions.

A property that is under-rented may still show positive cash flow, but it may be underperforming relative to its potential.

Maintenance Planning

Recurring repairs may indicate that a system or appliance should be replaced rather than repaired repeatedly.

For example, repeated HVAC service calls may justify evaluating replacement. Frequent plumbing repairs may indicate older supply lines, drainage issues, tenant misuse, or deferred maintenance.

Property Manager Evaluation

Owner statements help landlords evaluate whether the manager is controlling costs, collecting rent, enforcing lease terms, documenting repairs, and communicating clearly.

Strong reporting does not guarantee strong management, but weak reporting often creates avoidable risk.

Hold, Sell, or Reposition Decisions

If the property produces weak cash flow over several quarters, the owner may need to revisit the investment plan.

The problem may be solvable through rent increases, better management, repairs, refinancing, or repositioning. Or the property may no longer fit the owner’s goals.

Owner statements provide the financial history needed to make that decision rationally.

Best Practices for Reviewing Owner Statements

Landlords should use a simple repeatable process each month.

Review the Statement Promptly

Read the statement within a few days of receiving it. Errors are easier to correct while the month is still fresh.

Save Every Statement

Store statements by property and year. Keep invoices, leases, inspection reports, tenant ledgers, and tax documents in the same digital filing system.

Reconcile Owner Distributions

Compare the owner distribution on the statement to the actual deposit in the owner’s bank account.

If the amounts do not match, ask why.

Track Key Numbers

At minimum, landlords should track:

Monthly rent collected

Total operating expenses

Maintenance and repairs

Management fees

Owner distribution

Reserve balance

Owner contributions

Ending balance

This can be done in a spreadsheet. The goal is to spot patterns, not to create unnecessary administrative work.

Ask Questions in Writing

If something is unclear, ask by email or through the owner portal. Written communication creates a record and reduces confusion.

Review Quarterly and Annually

Monthly statements show short-term activity. Quarterly and annual reviews show trends.

A quarterly review is especially useful for comparing maintenance costs, vacancy, collections, and net cash flow.

Final Thoughts

Rental property owner statements are one of the landlord’s most important oversight tools. They show how the rental is performing, how the property manager is handling funds, and whether the investment is producing the expected results.

A good owner statement should clearly show rent collected, other income, expenses, management fees, leasing fees, reserves, owner contributions, owner distributions, and ending balances. It should be easy to understand and supported by invoices, ledgers, and related reports when needed.

Landlords should pay close attention to vague expenses, missing invoices, unexplained rent shortfalls, repeated owner contributions, negative balances, inconsistent fees, and delayed reporting. These issues do not always prove mismanagement, but they do require explanation.

The strongest owners do not simply check the monthly deposit. They read the statement, compare it to the lease and management agreement, track trends, and ask clear questions when something does not make sense.

A rental property may be professionally managed, but the investment still belongs to the owner. Reviewing rental property owner statements carefully is one of the simplest ways to protect that investment and make better long-term decisions.

Are You Looking To Connect With Property Owners, Landlords, and Real Estate Investors?

Grow your business by connecting with property professionals with our cost-effective advertising options.